By Rick Walker, Financial Planner & CPA, and Kimberlee Clark, Financial Planner – NaplesWealthStrategies.com

Throughout our careers as a financial planners & all of Rick’s years as a CPA, we have regarded the payment of taxes as an awful byproduct of success in life. Whether it is earning a sizeable income, or having a large gain on investment, writing that check to the IRS can make you cringe, bringing stress and anxiety.

Today, we are addressing a tax problem that has been brewing for several years. More & more people are seeing their traditional IRA & 401(k) balances grow to larger amounts. Years down the road, whether withdrawing during your lifetime, or passing on to heirs, the taxes imposed can be shockingly enormous.

Why Conversions Matter More than Ever!

A Roth conversion is one of the most powerful tools available for creating long-term tax efficiency. It allows investors to move money from pre-tax accounts—like a Traditional IRA or 401(k)—into a Roth IRA. Taxes are paid upfront on the converted amount, unlocking substantial long-term benefits.

First, we will address the impact during your lifetime, and secondly, we will address the impact to your heirs under the 10 Year Rule for beneficiaries.

During your lifetime:

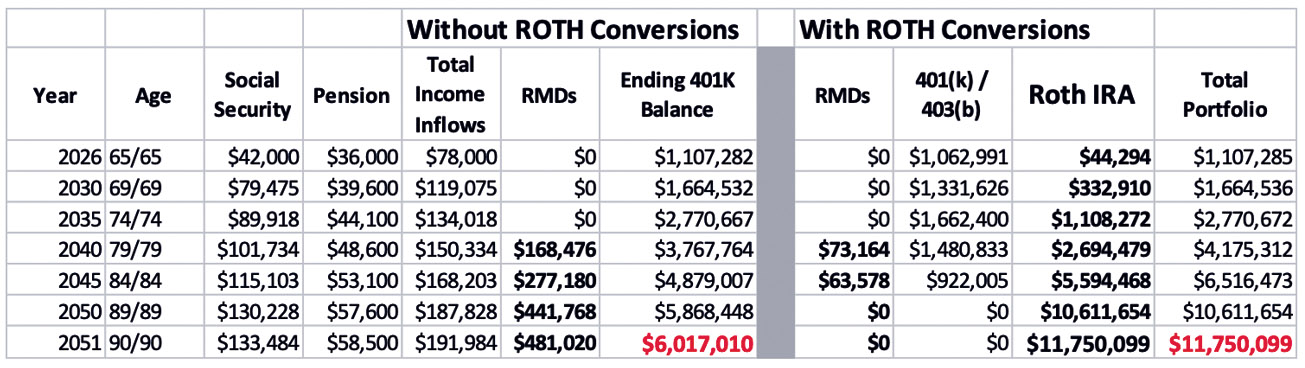

Tax-Free Growth and No RMDs

Once assets enter a Roth IRA, investments compound without future income taxation, and qualified withdrawals are entirely tax-free. Paying taxes today on a smaller balance is often far more advantageous than paying taxes later on a much larger account value. Additionally, Roth IRAs eliminate lifetime Required Minimum Distributions (RMDs), which force Traditional account holders to take taxable withdrawals starting at age 73 or 75. These mandatory distributions can create a “tax snowball,” pushing retirees into higher tax brackets, increasing Medicare premiums (IRMAA surcharges), and causing more Social Security income to become taxable.

Strategic Execution

A Roth conversion acts as a hedge against future tax increases. Investors can proactively recognize income during “sweet spot” years when their tax bracket is temporarily lower, such as:

* Early retirement before Social Security begins

* Temporary drops in income

* Stock market downturns

Generational Wealth Transfer

Effective beginning January 1, 2020, when a person passes away and leaves their retirement account balances to a non-spousal heir, the entire sum must be withdrawn by the 10th year after death.

This area of estate planning is where Roth conversions provide tremendous value with regard to taxes. Since non-spousal beneficiaries inheriting traditional accounts must fully distribute those funds within 10 years, it can result in paying very large amounts of ordinary income tax during their peak earning years. Conversely, inherited Roth IRAs are distributed tax-free, allowing families to transfer wealth across generations far more efficiently.

Just a quick example: A surviving spouse passes at age 89, leaving a $3 million IRA equally to two children, ages 58 & 60. Each of these children would have to withdraw their half within the 10 years after death. If the balances didn’t grow and equal amounts were taken each of the ten years, which would be additional ordinary income of $150,000 to recognize each year, generally at an effective tax rate above 22%. But that isn’t realistic, because the balances tend to grow and heirs tend not to withdraw in the early part of the 10 year window. A more likely situation is that the money is not withdrawn in the first 5 years. Rather it grows from the original $1.5 million, and each child is withdrawing $3 million over the last 5 years of the window. That becomes $600,000 and will bridge the 35% tax bracket. (Approximately and additional $185,000 in federal tax just on the IRA withdrawal amount of $600,000). If your heirs live in a location that imposes

State Income Tax, we would suggest looking at Florida residency. It may be worthy the consider as it just may pay for itself!

Why Guidance Matters

Timing and execution are critical. At Naples Wealth Strategies, we build personalized, multi-year strategies tailored to your unique retirement timeline, income needs, and long-term goals. We help you convert the right amount at the right time, maximizing lifetime tax savings and keeping you in control of your financial future

The most important thing to understand is that your situation is unique, and will be different from your brother, sister, neighbor, or best friend. That is why you must look at a customized analysis & financial projection that incorporates your income, assets, & family structure.

239-434-6613

4933 N. Tamiami Trail, Suite 202, Naples, FL 34103

NaplesWealthStrategies.com